The order‑to‑cash (O2C) cycle, the sequence from taking a customer order to collecting cash is the lifeblood of every company. Yet many organizations still rely on manual, siloed processes that clog cash flow and drain staff resources. When customer orders and invoices are processed by hand, it takes roughly 15–20 minutes per invoice, and approval cycles can stretch across multiple days. Meanwhile, high Days Sales Outstanding (DSO) locks up working capital; an average company sees over $0.56 million in cash tied up for every single-day increase in DSO. These friction points create real business pain: delayed revenue recognition, poor visibility into receivables and customer frustration.

Recent advances in artificial intelligence (AI) and integration‑platform‑as‑a‑service (iPaaS) technologies offer a way out. AI extracts data, validates it and makes decisions at machine speed, while iPaaS provides a unified layer that connects disparate systems, Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), e‑commerce storefronts and payment gateways without heavy IT overhead. Together they promise to cut processing times, improve accuracy and unlock working capital. This blog explores how AI‑powered order‑to‑cash integration with iPaaS delivers tangible results for modern businesses, and why embracing this combination is becoming a strategic necessity.

The Hidden Pain Points of a Manual O2C Process

Before integration and automation, the order-to-cash cycle is riddled with inefficiencies that quietly erode revenue, cash flow and customer trust. Businesses typically face:

- Slow order entry due to manual data keying from emails, PDFs and portals

- Frequent errors caused by duplicate entries, mismatched SKUs or incorrect pricing

- Delayed invoicing leading to longer DSO and cash-flow strain

- Poor visibility across orders, fulfilment, payments and collections

- Fragmented systems (ERP, CRM, e-commerce, finance) with no real-time sync

- High operational cost as teams spend hours reconciling data manually

- Customer frustration from shipping delays, incorrect invoices and slow dispute resolution

Steps of the O2C process

- Order management: Orders arrive via e‑commerce sites, sales teams or EDI feeds. Manual entry risks errors and delays. AI‑enabled automated order processing reads purchase orders using optical character recognition (OCR) and validates data, reducing manual intervention.

- Credit management: Assessing a customer’s creditworthiness is vital to prevent bad debt. AI models analyse transaction history, industry data and behavioural signals to generate dynamic credit limits, thereby reducing risk and accelerating approvals.

- Order fulfilment: Coordinating inventory, logistics and third‑party logistics (3PL) providers requires real‑time data. Integrations via iPaaS ensure orders flow seamlessly to warehouse management systems and shipping carriers.

- Invoicing and billing: Manual invoice creation is time consuming and prone to errors. Automated solutions cut processing time by 70–90% and reduce costs by about 70%, while ensuring compliance with varying e‑invoice formats.

- Payment processing: Customers pay through different methods (bank transfer, card, digital wallet). iPaaS connectors route payments to accounting systems, capturing transaction fees and remittance data.

- Cash application: Matching incoming payments to open invoices often involves reconciling partial or missing remittance data.

- Collections and dispute resolution: Predictive collections software groups customers by likelihood to pay and recommends personalized outreach, while AI‑powered dispute resolution categorises deductions and recommends evidence.

- Reconciliation and reporting: Consolidated data feeds into dashboards for close management.

Without automation and integration, each stage becomes a manual bottleneck. High DSO saps liquidity, while disconnected systems create errors, duplicate data entry and little visibility. A modernised O2C process closes these gaps and fosters efficiency across the entire revenue cycle.

Why AI + iPaaS Is the Future of O2C

The future of the O2C cycle is intelligent, connected and adaptive. AI technologies such as machine learning, natural language processing (NLP), robotic process automation (RPA) and generative AI allow systems to understand documents, recognise patterns and make decisions. An iPaaS provides a cloud‑based platform that connects disparate systems (ERP, CRM, e‑commerce, payment gateways, logistics) using prebuilt connectors and low‑code workflows. By moving data in real time and orchestrating multi‑step processes across applications, iPaaS eliminates swivel‑chair integration and reduces IT burden. Key benefits include:

- Low‑code/no‑code integration: Business users can build and modify workflows without extensive programming, speeding up time‑to‑value and reducing dependence on scarce IT resources.

- Unified data governance: Centralized integration ensures consistent data models and security controls across applications, addressing compliance requirements and enabling a single source of truth.

- Scalability and resilience: iPaaS platforms offer high availability (often 99.9% or more) and elasticity, allowing organizations to handle seasonal spikes without performance degradation.

- Monitoring and analytics: Built‑in dashboards track integration health, data flows and exception handling, providing transparency and facilitating continuous improvement.

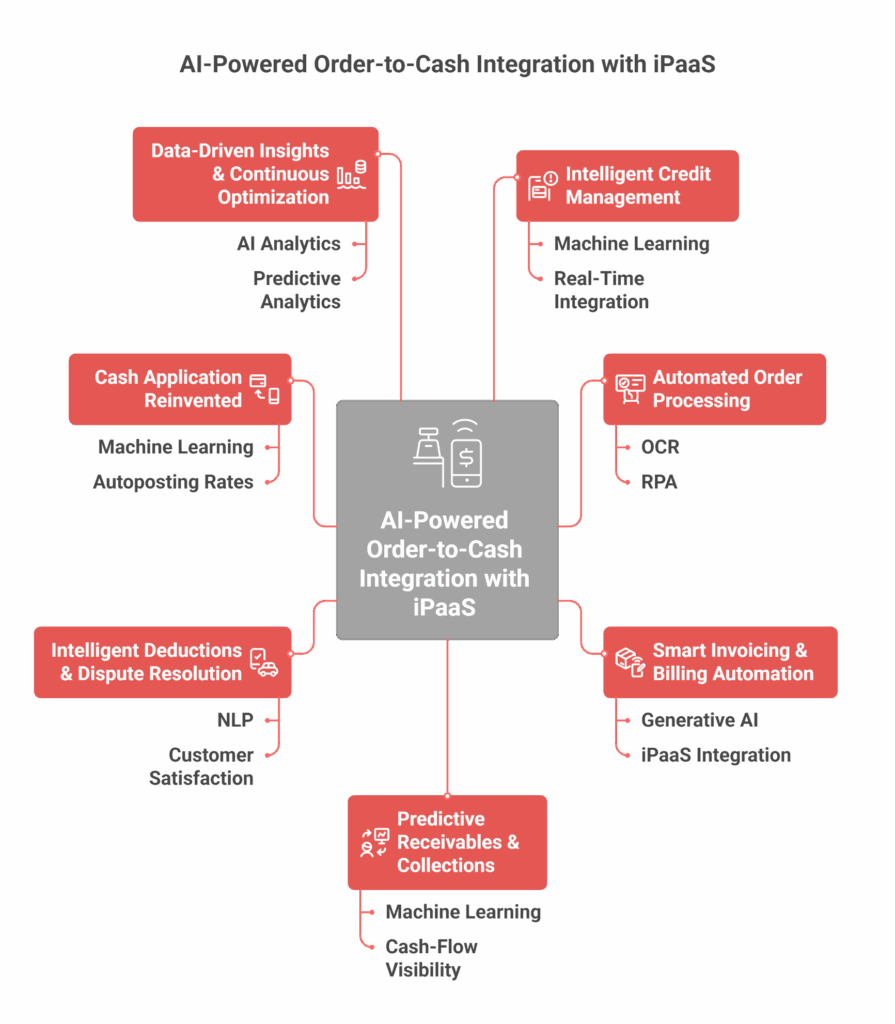

Core Components of an AI‑Powered, iPaaS‑Enabled O2C Platform

A high‑performing order‑to‑cash platform leverages AI and iPaaS to automate every stage of the cycle. The following components illustrate how each part works in practice and where the value is delivered.

Intelligent Credit Management

Traditional credit assessments rely on static financial statements and manual checks, which struggle to keep pace with dynamic markets. Intelligent credit management uses machine learning to evaluate customer behaviour, transaction history, external risk data and macroeconomic indicators. This produces dynamic credit scores that adapt to current conditions, enabling more accurate credit limits and reducing bad‑debt write‑offs. By proactively flagging risky accounts and recommending appropriate payment terms, AI shortens approval cycles and accelerates order processing. Additionally, real‑time integration via iPaaS pulls data from credit bureaus, ERP and CRM systems, ensuring that credit decisions are based on the latest information.

Automated Order Processing

Capturing and validating orders manually is slow and error‑prone. Automated order processing combines OCR, AI and RPA to read purchase orders, extract key details and compare them against product catalogues and contract terms. When orders arrive in various formats, PDF, email, portal uploads, AI can standardise them and route them through prebuilt workflows. iPaaS connectors send validated orders to ERP, inventory and warehouse systems in real time, enabling timely fulfillment and reducing the risk of backorders or duplicate shipments.

Smart Invoicing & Billing Automation

Creating invoices manually is labour‑intensive and prone to errors, particularly when each customer has unique billing requirements. Smart invoicing and billing automation uses AI to validate invoice data against purchase orders (POs), contracts and delivery notes. Generative AI personalizes invoice communications and reminders, adjusting tone and content based on a customer’s payment history and industry norms. When integrated through iPaaS, invoices flow seamlessly into accounting, CRM and customer portals, ensuring consistency and timely delivery.

Predictive Receivables & Collections

Collections teams often rely on static ageing reports, making it difficult to prioritize accounts and anticipate late payments. Predictive receivables and collections harness machine learning to classify customers by likelihood to pay and recommend targeted outreach strategies. These capabilities improve cash‑flow visibility, allow earlier intervention and reduce friction with customers.

Intelligent Deductions & Dispute Resolution

Deductions, short payments and disputes often swamp finance teams, delaying cash collection and straining customer relationships. Intelligent deductions and dispute resolution applies NLP and machine learning to categorise deduction reasons (pricing errors, damaged goods, invoice discrepancies), link them to supporting documents and recommend actions. Automating deduction triage frees collectors to focus on strategic negotiations and customer satisfaction.

Cash Application Reinvented

Applying payments to invoices is traditionally one of the most time‑consuming tasks in accounts receivable. Payments arrive via multiple channels, and remittance information is often incomplete. AI‑driven cash applications use machine learning to match payments with open invoices by analysing amounts, payment patterns and historical data. Autoposting rates often exceed 90%, enabling real‑time visibility into customer balances and lowering unapplied cash. When integrated via iPaaS, payment data flows directly from banks and payment gateways into ERP and accounting systems, eliminating file uploads and manual reconciliation.

Data‑Driven Insights & Continuous Optimization

Modern finance leaders need more than static reports; they require predictive insights and scenario‑planning capabilities. Data‑driven insights and continuous optimization combines AI analytics with integrated data to provide real‑time dashboards and “what‑if” forecasting. Consolidated dashboards built on iPaaS unify data across ERP, CRM and external sources, offering a single version of truth. Coupled with predictive analytics, managers can simulate the impact of new discount policies, credit terms or sales campaigns on cash flow, enabling continuous improvement.

Overcoming Challenges & Best Practices

Implementing an AI‑powered, iPaaS‑enabled O2C platform is transformative but not without challenges. Legacy ERP systems, fragmented data, regulatory compliance and change management can impede progress. To succeed, organizations should follow these best practices:

- Define a clear vision and secure executive sponsorship. Align O2C modernisation with strategic goals such as cash‑flow improvement, customer experience and operational efficiency.

- Assess current maturity and identify friction points. Map existing processes, quantify manual work and pinpoint stages with high error rates or delays.

- Establish data governance. Develop a unified data model, enforce privacy controls and ensure compliance with regulations like GDPR or local tax laws.

- Select the right technology stack. Evaluate AI/ML engines, OCR/NLP tools, RPA platforms, real‑time dashboards and, importantly, an iPaaS that offers prebuilt connectors and low‑code capabilities. Avoid vendor lock‑in and prioritise scalability and security.

- Pilot, measure and scale. Start with a well‑defined pilot (e.g., invoice automation), track metrics such as DSO reduction, processing time and accuracy, then roll out to other stages.

- Ensure governance, ethics and bias monitoring. AI models can carry biases; establish oversight processes to validate credit decisions and collection strategies.

- Drive change management. Train employees, create a centre of excellence and communicate benefits to encourage adoption. Focus on transforming roles so staff can handle higher‑value tasks like customer relationship management and strategic analysis.

By adhering to these steps, organizations can mitigate risks, accelerate adoption and realize the full benefits of AI‑enabled O2C transformation.

Why Choose Burq iPaaS for AI‑Driven Order‑to‑Cash

Implementing AI across the O2C cycle requires a robust integration backbone. Burq iPaaS provides a unified platform designed specifically for commerce‑centric enterprises. Key differentiators include:

- Low‑code/no‑code integration: Business users can create workflows that connect ERP, CRM, e‑commerce platforms, payment gateways and 3PL systems without heavy coding. Prebuilt connectors accelerate deployment and reduce IT bottlenecks.

- Pre‑built order‑to‑cash automation packs: Burq offers templates to automate order entry, invoicing, cash application and collections. These templates incorporate best practices and can be tailored to specific industries.

- Scalable and reliable infrastructure: During peak shopping periods like Black Friday/Cyber Monday, Burq customers experience 100% uptime, ensuring orders and payments flow smoothly. Auto‑scaling ensures performance even as transaction volumes surge.

- Unified data and monitoring: Burq centralises data governance and offers dashboards to monitor data flows, integration health and exceptions. This visibility simplifies compliance and accelerates issue resolution.

- Security and compliance: The platform is built with enterprise‑grade security, including encryption at rest and in transit, role‑based access controls and support for regional data residency requirements.

- Industry‑proven results: Burq’s customers, ranging from direct‑to‑consumer brands to global distributors, report improved order fulfilment, faster invoicing and reduced DSO. For example, connected storefront‑to‑ERP integrations have reduced manual order entry and enabled same‑day invoicing, while real‑time payment updates give finance teams immediate visibility into cash receipts.

By choosing Burq iPaaS, business leaders gain a foundation for AI‑powered order‑to‑cash integration that is agile, reliable and built for modern commerce. Whether you operate an e‑commerce storefront, a subscription service or a wholesale distribution network, Burq enables you to connect, automate, centralise and monitor your revenue processes at scale.

Conclusion & Next Steps

The order‑to‑cash cycle is no longer a back‑office function; it is a strategic driver of growth, liquidity and customer satisfaction. Manual processes and siloed systems create high DSO, delayed cash application and poor visibility. By combining AI and iPaaS, organizations automate data extraction, decision‑making and integration across ERP, CRM, e‑commerce and payment systems.

To stay ahead, companies must adopt a platform that combines intelligent automation with flexible, scalable integration. Burq iPaaS offers this foundation, delivering low‑code connectivity, pre‑built automation packs and robust monitoring that help you realize rapid ROI.

The next step is simple: evaluate your current O2C process, identify bottlenecks and explore how AI and iPaaS can transform them. Contact Burq to schedule a personalized demo and discover how your organization can unlock cash flow, enhance customer experience and gain a competitive advantage through AI‑powered order‑to‑cash integration.

FAQs

How does AI improve the order-to-cash cycle?

AI automates data capture, decision-making, and document validation across order entry, invoicing, collections, and cash application. This reduces errors, speeds up processing, and helps you collect cash faster.

Why do companies need iPaaS for O2C automation?

iPaaS connects ERP, CRM, e-commerce, and payment systems into one flow. Without it, automation breaks due to data silos. Platforms like Burq iPaaS ensure real-time sync and smooth multi-system workflows.

Can AI reduce Days Sales Outstanding (DSO)?

Yes. Automated invoicing, predictive collections, and AI-driven cash application accelerate cash

What is the benefit of combining AI with iPaaS?

AI handles intelligence (like recognition, classification, forecasting), while iPaaS handles connectivity. Together, they deliver end-to-end automation that removes manual steps across the entire O2C lifecycle.

How does Burq iPaaS support AI-powered O2C automation?

Burq iPaaS offers prebuilt O2C workflows, low-code integration, real-time monitoring, and reliable uptime. It simplifies connecting ERP, CRM, storefronts, and payment gateways so AI can run at full potential.

What results can businesses expect from AI-enabled O2C transformation?

Organizations typically see faster order processing, 70–90% lower invoice effort, increased autoposting accuracy, better cash-flow visibility, and fewer customer disputes—all driving higher operational efficiency.